Health Insurance in Pakistan – An Overview by Nadeem R. Malik

9/23/20254 min read

Health Insurance in Pakistan – an overview by Nadeem R. Malik

The rising cost of healthcare in Pakistan poses a severe risk to household financial stability, making health insurance a critical, rather than optional, safeguard. This analysis delves into the necessity of coverage, the systemic hurdles preventing its uptake, and proposes strategic solutions to foster a healthier and more economically protected population.

Why Health Insurance?

Health insurance serves as a critical financial safeguard, protecting households from the devastating expenses of medical treatment and preventing a health emergency from precipitating financial collapse.

1. Deteriorating Public Healthcare System Pakistan's public healthcare system is overburdened and under-resourced.

Overcrowding: Government hospitals face severe overcrowding, resulting in long waits for consultations, diagnostics, and surgeries.

Variable Quality: Shortages of medicines, a lack of advanced equipment, and inconsistent quality of care are common challenges.

Basic Care Focus: The system is geared towards routine healthcare, often struggling with complex, specialized treatments.

Health insurance provides a gateway to private hospitals, ensuring timely access to higher-quality care.

2. Rising Prevalence of Lifestyle Diseases Pakistan is experiencing a sharp rise in Non-Communicable Diseases (NCDs):

Cardiovascular Diseases: Increasing rates of heart attacks and hypertension.

Diabetes: One of the highest national rates globally.

Cancer: Rising incidence of various cancers.

These chronic conditions require long-term, expensive management. Insurance covers these ongoing costs, making sustainable care possible

3. Financial Protection & Risk Management without insurance, families facing a health crisis are often forced to:

Deplete savings meant for education or retirement.

Sell assets like property or jewellery.

Take on high-interest loans.

Rely on charity.

Health insurance transforms an unpredictable, catastrophic expense into a manageable, predictable premium. It is the cornerstone of sound financial risk management.

4. Access to a Wider Network & Quality Care Insurers provide access to extensive panels of hospitals and specialists.

Choice: Freedom to choose where you receive treatment.

Cashless Treatment: Direct billing with network hospitals eliminates large out-of-pocket payments.

Quality Assurance: Partnerships with reputable hospitals offer confidence in the standard of care.

5. Peace of Mind The psychological security of knowing your family is protected reduces stress and allows focus on recovery, not financial panic.

Who Needs It Most?

The Sole Breadwinner: Protects family stability if illness halts income.

Parents & Elderly Family Members: Covers more frequent healthcare needs.

Those with Family Histories of Chronic Disease: A proactive step for at-risk individuals.

Anyone Without Significant Savings: For the majority without a financial cushion, it is a necessity.

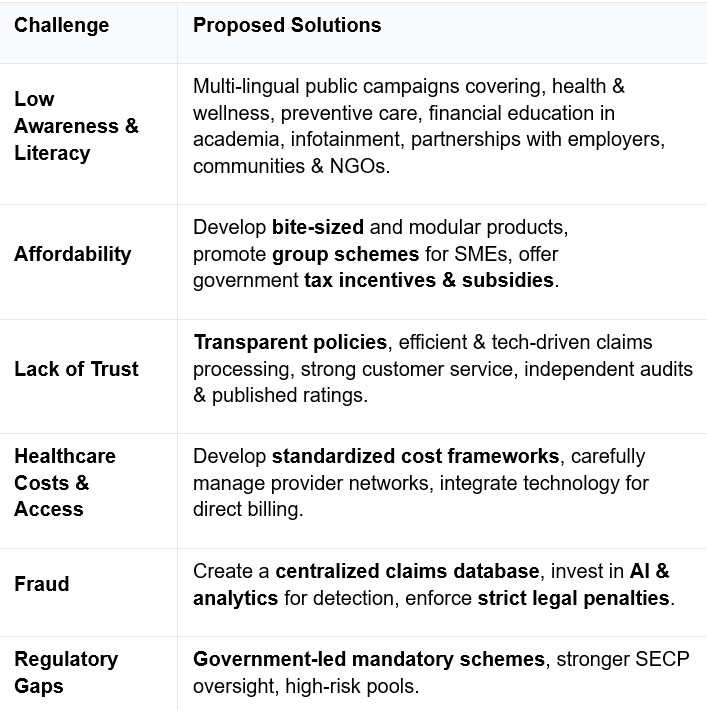

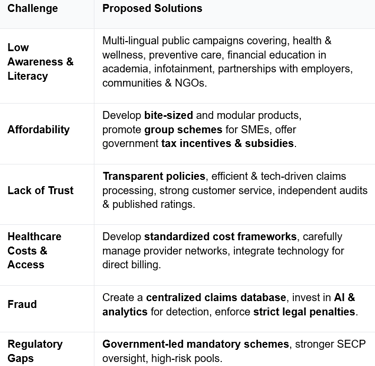

Key Challenges faced by the Health Insurance Industry

The potential is enormous, but the path is full of systemic hurdles.

1. Economic & Affordability Challenges

Low Disposable Income: For many, insurance is a luxury after basic needs.

High Premium Costs: Comprehensive coverage is expensive, pricing out a large segment of the market.

Economic Instability: Inflation and currency devaluation increase the cost of medical imports, driving up claim costs and premiums.

2. Regulatory & Structural Hurdles

Low Insurance Penetration & Density: A fundamental lack of understanding, realization of it’s need and trust in insurance products.

Evolving Regulatory Framework: The SECP has undertaken a series of initiatives and put forward recommendations aimed at developing the health insurance ecosystem, an effort which remains ongoing.

Unfavourable Taxation: Lack of attractive tax relief or incentives for individuals or corporations, unlike in many other countries.

3. Healthcare System Infrastructure

Inadequate Provider Network: Quality healthcare is concentrated in major cities, making nationwide network establishment difficult.

Quality & Cost Variation: Huge disparities in care and pricing complicate risk assessment and premium calculations.

Lack of Data: A severe shortage of reliable data on disease prevalence and treatment costs makes accurate product pricing a challenge.

4. Cultural & Behavioural Factors

Lack of Trust: Mistrust fuelled by perceptions of complex procedures and claim denials.

Reliance on Family Support: A cultural preference for familial support over formal insurance mechanisms.

Preference for Out-of-Pocket Payments: A habit of paying for healthcare as needed, rather than planning for it.

5. Operational & Fraud-Related Risks

Claims Fraud: Includes provider overcharging and policyholder misrepresentation, requiring costly audit systems.

Administrative Complexity: Capital-intensive processes for provider management, claims processing, and customer service.

Immature TPA Ecosystem: Underdeveloped Third-Party Administrator industry increases the operational burden on insurers.

The Way Forward: A Collaborative Blueprint

Overcoming these challenges requires a multi-stakeholder approach.

The Government's Pivotal Role:

Mandatory Schemes: Making insurance mandatory for formal/documented sector workers would create a massive, stable risk pool providing critical mass to insurers to come up with more affordable products, leveraging economies of scale

Strengthening Regulation: The SECP must continue to enhance its framework to protect consumers as well as the Insurance Industry to ensure market stability.

A Call to Action: The Time for Collaboration is Now

The recent SECP report on Pakistan's Healthcare Ecosystem highlights a critical warning: Group Health Insurance coverage declined from 8.2 million lives in 2019 to 6.5 million in 2023. This represents a shrinking safety net for millions and a clear call to action.

Seizing the Opportunity:

Formal Sector Growth: Registered businesses with FBR exceeding 12.5 million (increase of 5.3 million in 3 years), a Compulsory Occupational Health Insurance (COHI) scheme proposed by SECP, incentivized by tax credits, is a viable near-term solution to reverse this decline.

A Major Untapped Opportunity: With a workforce of 57.2 million (more than half self-employed) and an individual retail health insurance market that currently serves only 31,000 individuals (contributing only1% of private sector health insurance premiums), there is a clear and compelling opportunity to capture a new, large segment of consumers.

The Freelancer Economy: Pakistan's 2-3 million freelancers, a major source of foreign remittances ($2.6 billion in FY23), represent a new, digitally savvy demographic ripe for tailored more sophisticated insurance products through online distribution channels

The foundation for a more resilient and inclusive healthcare safety net exists. To build it, timely and deliberate collaboration among government, insurers, healthcare providers, and the public is essential. By working together, we can shift the perception of health insurance from a luxury to a national necessity.

The writer is a well known insurance and takaful senior and can be contacted on: nadeem.malik@bullsnbulls.com

#LOUG